.jpg)

Expanding your business across borders opens doors to new opportunities, but it also comes with challenges, particularly with payments. International sales introduce added complications, different currencies, fluctuating exchange rates, hidden bank charges, and compliance issues, which can eat into your profits if you aren’t careful. The good news is that with the right tools and strategies, managing cross-border transactions can be seamless, secure, and cost-effective. The key to staying ahead is using the right systems and processes to simplify transactions and protect your revenue, all while keeping global clients happy.

In this guide, we’ll walk through practical steps on how to handle international payments like a pro, so sit back, relax, and take notes.

Step 1: Understand the Basics of Cross-Border Payments

Before managing cross-border payments effectively, it’s important to understand what sets them apart from local transfers. A cross-border payment simply means money moving between two people or businesses in different countries. Unlike domestic transfers, these involve multiple layers such as currency conversion, intermediary banks, and international regulations, which can make them slower and more expensive.

The main players in this process are:

- Banks, which handle most traditional transfers but often charge high fees.

- Payment processors that move money between countries on behalf of businesses.

- Fintech platforms. These have disrupted the space by offering faster, cheaper, and more transparent services.

For example, think of a freelancer in Lagos who’s been hired by a client in New York. When the client pays, the transaction doesn’t just “go through.” It passes through currency conversion, checks for compliance, and sometimes intermediary banks or card networks before reaching the freelancer’s account. Understanding these moving parts helps you spot where delays or fees may appear and how to avoid them.

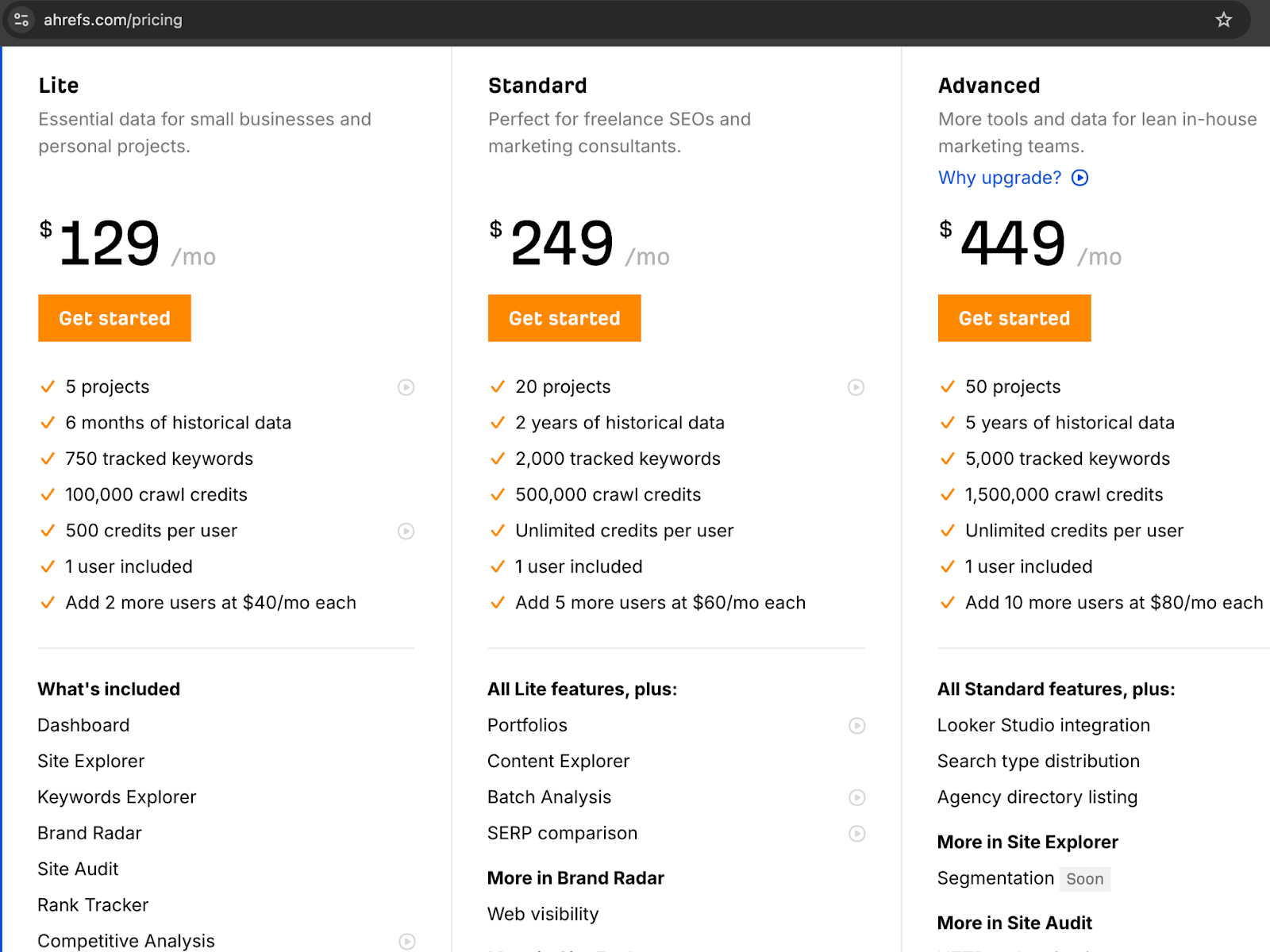

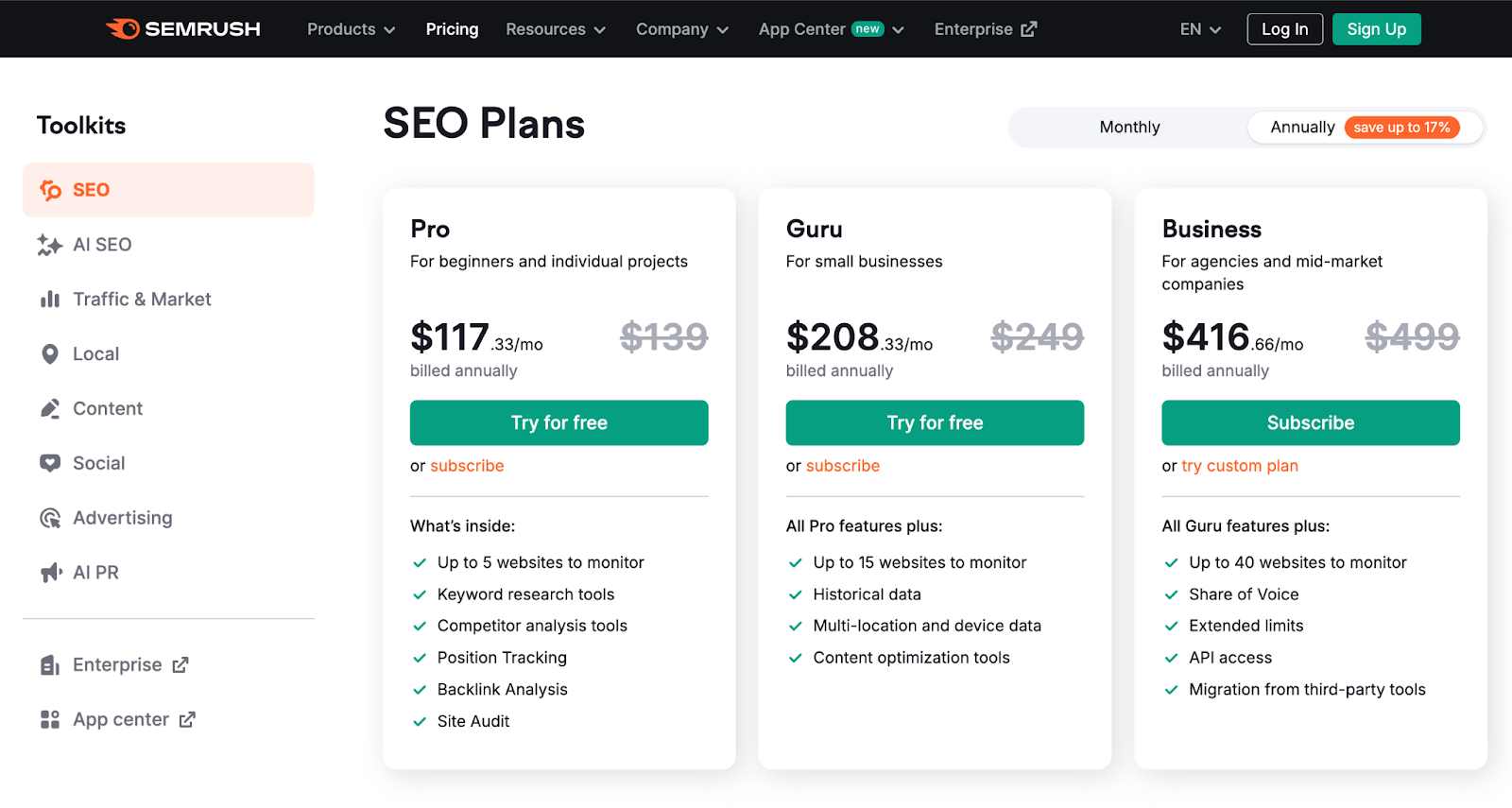

Step 2: Choose the Right Payment Platform

Not all payment methods are created equal. Traditional banks are reliable but often slow and expensive for cross-border transfers. That’s why many freelancers, small businesses, and service providers turn to digital alternatives.

Here are a few options worth considering:

Wise (formerly TransferWise) – Known for transparent fees and real exchange rates.

Payoneer – Popular with freelancers and marketplaces like Upwork or Fiverr.

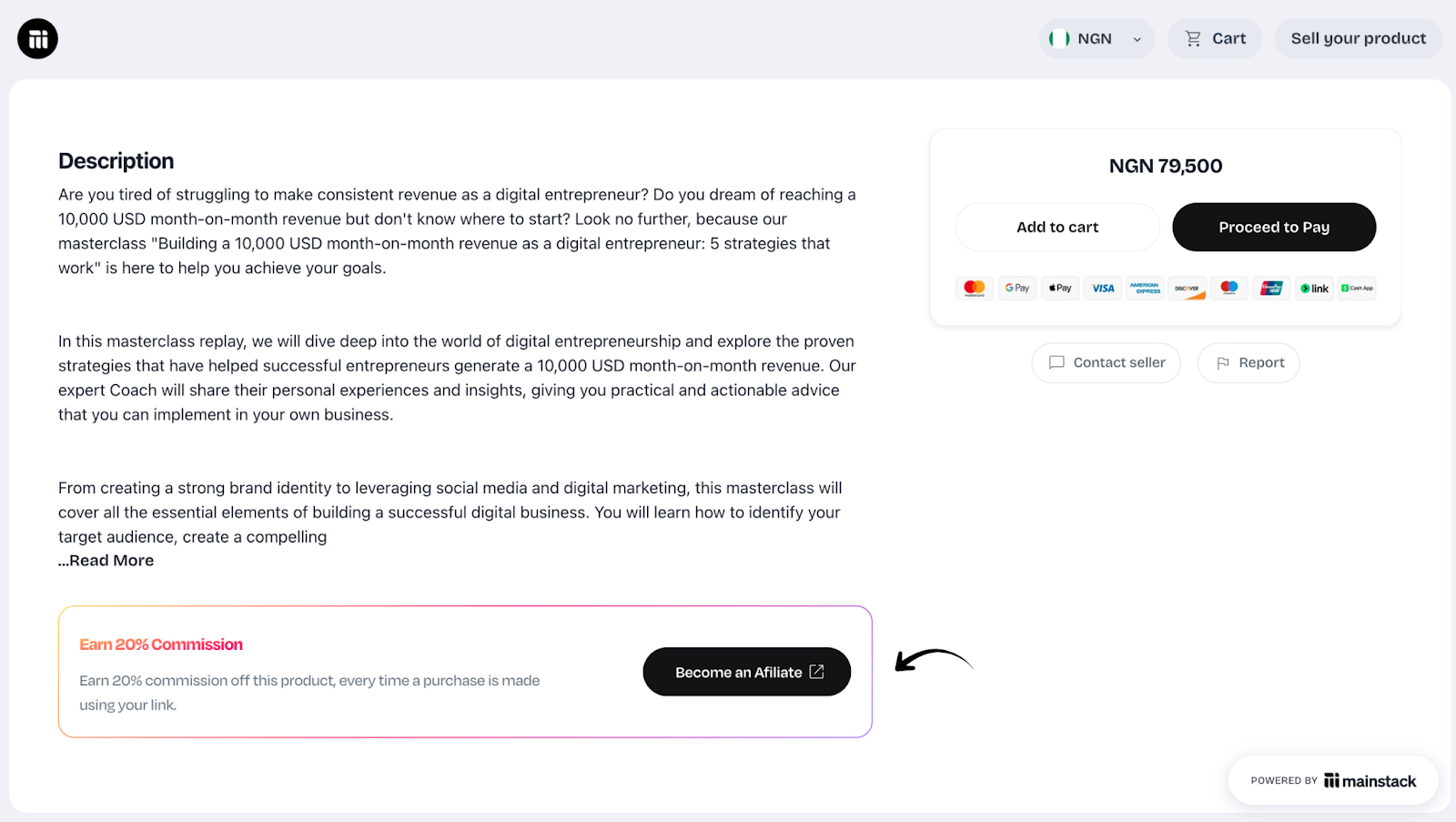

Mainstack – An all-in-one platform for African creators, service providers, and entrepreneurs, offering multi-currency support, fast payouts, and low fees.

PayPal – Widely recognized, easy to set up, but can be expensive with fees.

Flutterwave – Strong in African markets, supports multiple currencies and global payouts.

Pro tip: If you’re looking for a seamless experience, consider platforms like Mainstack that combine multiple currency integrations, low fees, and quick transfer speeds. They save you both time and money.

Step 3: Prioritize Security and Compliance

Cross-border payments are more than just the money or day-to-day transactions. They involve regulations. Every country has financial compliance rules to prevent fraud and money laundering, so it’s essential to use providers that take security seriously.

To stay safe, be sure your account with whichever platform you decide to use meets the following requirements :

- KYC (Know Your Customer) – Verify your identity with documents like passports or IDs. This protects both you and your clients.

- AML (Anti-Money Laundering) compliance – Regulated providers monitor suspicious activity to keep your funds secure.

- Account security – Always enable multi-factor authentication and monitor your accounts for unusual activity.

For example, if you’re working with a client overseas, using a regulated platform like Wise, Payoneer, or Mainstack ensures the transaction meets compliance standards. This not only protects your earnings but also builds trust with clients who want to know their money is moving through secure channels.

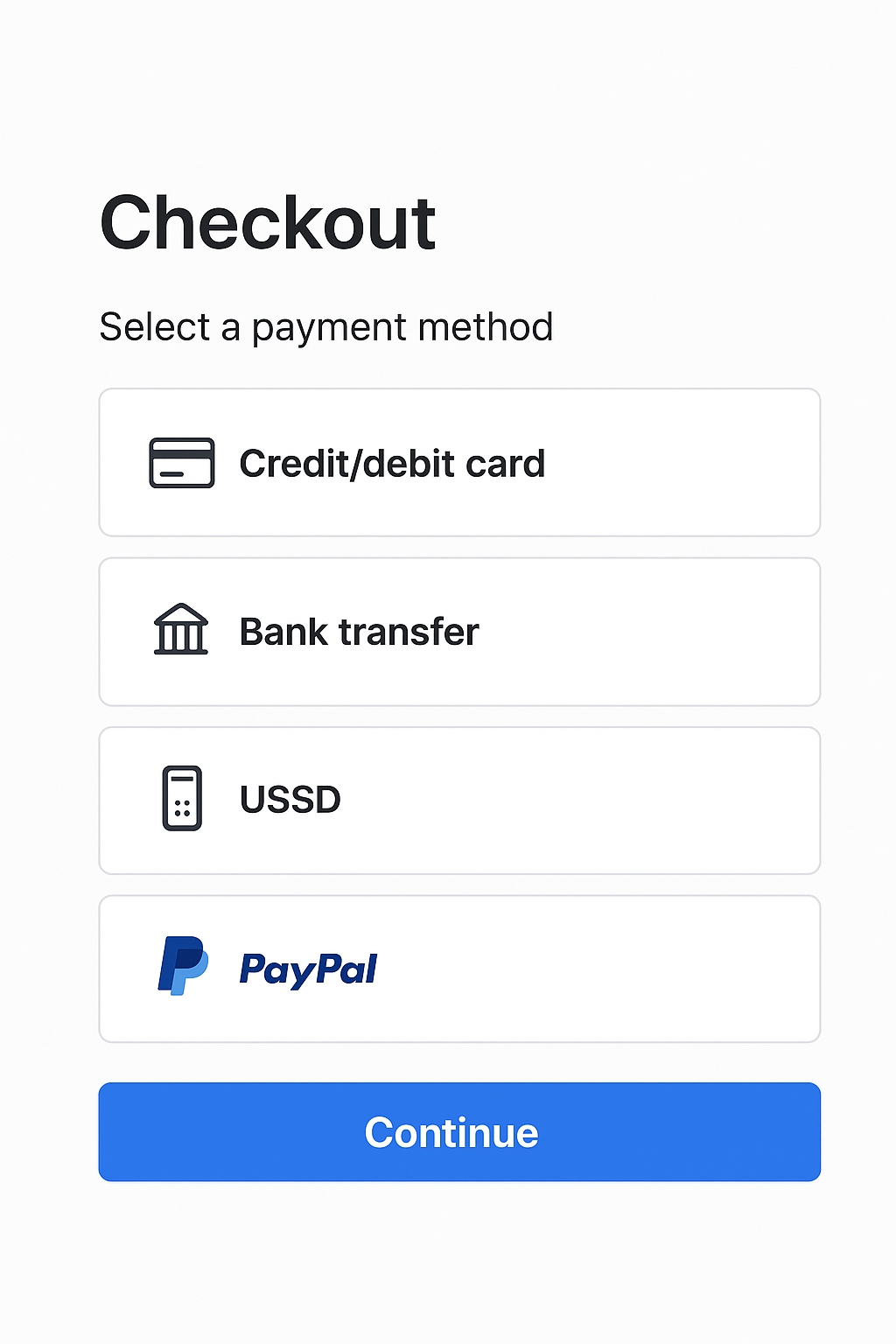

Step 4: Choose the Right Payment Methods for Your Audience

Different customers have different payment preferences, and this becomes even more important when you’re selling internationally. In some regions, cards dominate. In others, wallets like PayPal or mobile money are the norm. The goal is to reduce friction because if a buyer doesn’t see a familiar or trusted option at checkout, chances are they’ll abandon their cart.

Take time to research which payment methods are most trusted in the markets you’re targeting. For example, in the UK, debit cards and PayPal are very common, while in Nigeria, bank transfers and mobile money are widespread. Offering multiple options signals reliability and makes it easier for customers to complete their purchase without second-guessing.

Step 5: Make Currency Conversion Simple

One of the fastest ways to lose a customer is to make them calculate prices themselves. Imagine seeing an item priced in dollars when you’re used to paying in naira or pounds. It feels like extra work, and it raises doubt about the true cost or value of the item/service.

Customers prefer to pay in a familiar currency because it reduces uncertainty about exchange rates and makes the process more transparent. To avoid drop-offs in the sales funnel, use tools that automatically display prices in your customers’ local currency or allow them to switch easily at checkout. Many payment providers offer built-in conversion features, and some e-commerce platforms let you conveniently plug this in.

The goal here is transparency and flexibility. Customers should not only be able to make payment in their own currency, but should also know exactly what they’re paying without having to pull out a calculator. This flexibility not only removes friction but also signals that you understand and respect your clients’ needs.

Step 6: Keep Records & Stay Compliant

Collecting payments is only half the job; properly tracking them is another, and it’s just as important. Accurate records make it easier to manage cash flow, handle taxes, and quickly resolve any disputes. In many countries, businesses must also meet compliance requirements such as Anti–Money Laundering (AML) and Know Your Customer (KYC) regulations. Choosing platforms that automatically generate receipts and provide exportable transaction histories saves you time and also ensures you remain compliant.

Step 7: Build Trust Through Transparency

At the end of the day, clients and customers pay faster when they trust you. That means clear communication about fees, reliable delivery of products or services, and professional invoicing. By offering secure, well-known payment methods, your buyers/clients are reassured that their money is safe. Trust isn’t built overnight, but consistently smooth transactions go a long way toward repeat business and referrals.

Handling cross-border payments doesn’t have to be complicated. By choosing the right platforms, prioritizing security, simplifying currency conversion, and keeping accurate records, you can make the process seamless for both you and your clients. When payments are smooth, transparent, and flexible, you not only protect your revenue but also build trust that strengthens long-term relationships.

Start putting these steps into practice today, and you’ll be well on your way to handling international payments like a pro.

Expanding your business across borders opens doors to new opportunities, but it also comes with challenges, particularly with payments. International sales introduce added complications, different currencies, fluctuating exchange rates, hidden bank charges, and compliance issues, which can eat into your profits if you aren’t careful. The good news is that with the right tools and strategies, managing cross-border transactions can be seamless, secure, and cost-effective. The key to staying ahead is using the right systems and processes to simplify transactions and protect your revenue, all while keeping global clients happy.

In this guide, we’ll walk through practical steps on how to handle international payments like a pro, so sit back, relax, and take notes.

Step 1: Understand the Basics of Cross-Border Payments

Before managing cross-border payments effectively, it’s important to understand what sets them apart from local transfers. A cross-border payment simply means money moving between two people or businesses in different countries. Unlike domestic transfers, these involve multiple layers such as currency conversion, intermediary banks, and international regulations, which can make them slower and more expensive.

The main players in this process are:

- Banks, which handle most traditional transfers but often charge high fees.

- Payment processors that move money between countries on behalf of businesses.

- Fintech platforms. These have disrupted the space by offering faster, cheaper, and more transparent services.

For example, think of a freelancer in Lagos who’s been hired by a client in New York. When the client pays, the transaction doesn’t just “go through.” It passes through currency conversion, checks for compliance, and sometimes intermediary banks or card networks before reaching the freelancer’s account. Understanding these moving parts helps you spot where delays or fees may appear and how to avoid them.

Step 2: Choose the Right Payment Platform

Not all payment methods are created equal. Traditional banks are reliable but often slow and expensive for cross-border transfers. That’s why many freelancers, small businesses, and service providers turn to digital alternatives.

Here are a few options worth considering:

Wise (formerly TransferWise) – Known for transparent fees and real exchange rates.

Payoneer – Popular with freelancers and marketplaces like Upwork or Fiverr.

Mainstack – An all-in-one platform for African creators, service providers, and entrepreneurs, offering multi-currency support, fast payouts, and low fees.

PayPal – Widely recognized, easy to set up, but can be expensive with fees.

Flutterwave – Strong in African markets, supports multiple currencies and global payouts.

Pro tip: If you’re looking for a seamless experience, consider platforms like Mainstack that combine multiple currency integrations, low fees, and quick transfer speeds. They save you both time and money.

Step 3: Prioritize Security and Compliance

Cross-border payments are more than just the money or day-to-day transactions. They involve regulations. Every country has financial compliance rules to prevent fraud and money laundering, so it’s essential to use providers that take security seriously.

To stay safe, be sure your account with whichever platform you decide to use meets the following requirements :

- KYC (Know Your Customer) – Verify your identity with documents like passports or IDs. This protects both you and your clients.

- AML (Anti-Money Laundering) compliance – Regulated providers monitor suspicious activity to keep your funds secure.

- Account security – Always enable multi-factor authentication and monitor your accounts for unusual activity.

For example, if you’re working with a client overseas, using a regulated platform like Wise, Payoneer, or Mainstack ensures the transaction meets compliance standards. This not only protects your earnings but also builds trust with clients who want to know their money is moving through secure channels.

Step 4: Choose the Right Payment Methods for Your Audience

Different customers have different payment preferences, and this becomes even more important when you’re selling internationally. In some regions, cards dominate. In others, wallets like PayPal or mobile money are the norm. The goal is to reduce friction because if a buyer doesn’t see a familiar or trusted option at checkout, chances are they’ll abandon their cart.

Take time to research which payment methods are most trusted in the markets you’re targeting. For example, in the UK, debit cards and PayPal are very common, while in Nigeria, bank transfers and mobile money are widespread. Offering multiple options signals reliability and makes it easier for customers to complete their purchase without second-guessing.

Step 5: Make Currency Conversion Simple

One of the fastest ways to lose a customer is to make them calculate prices themselves. Imagine seeing an item priced in dollars when you’re used to paying in naira or pounds. It feels like extra work, and it raises doubt about the true cost or value of the item/service.

Customers prefer to pay in a familiar currency because it reduces uncertainty about exchange rates and makes the process more transparent. To avoid drop-offs in the sales funnel, use tools that automatically display prices in your customers’ local currency or allow them to switch easily at checkout. Many payment providers offer built-in conversion features, and some e-commerce platforms let you conveniently plug this in.

The goal here is transparency and flexibility. Customers should not only be able to make payment in their own currency, but should also know exactly what they’re paying without having to pull out a calculator. This flexibility not only removes friction but also signals that you understand and respect your clients’ needs.

Step 6: Keep Records & Stay Compliant

Collecting payments is only half the job; properly tracking them is another, and it’s just as important. Accurate records make it easier to manage cash flow, handle taxes, and quickly resolve any disputes. In many countries, businesses must also meet compliance requirements such as Anti–Money Laundering (AML) and Know Your Customer (KYC) regulations. Choosing platforms that automatically generate receipts and provide exportable transaction histories saves you time and also ensures you remain compliant.

Step 7: Build Trust Through Transparency

At the end of the day, clients and customers pay faster when they trust you. That means clear communication about fees, reliable delivery of products or services, and professional invoicing. By offering secure, well-known payment methods, your buyers/clients are reassured that their money is safe. Trust isn’t built overnight, but consistently smooth transactions go a long way toward repeat business and referrals.

Handling cross-border payments doesn’t have to be complicated. By choosing the right platforms, prioritizing security, simplifying currency conversion, and keeping accurate records, you can make the process seamless for both you and your clients. When payments are smooth, transparent, and flexible, you not only protect your revenue but also build trust that strengthens long-term relationships.

Start putting these steps into practice today, and you’ll be well on your way to handling international payments like a pro.

.png)

.png)