.jpg)

Price objections kill more sales than any other factor. A customer sees your $1,000 course, wants it, but can't justify the upfront cost. They leave. You lose the sale.

Mainstack's Pay-in-Tranches eliminates this barrier by splitting payments into 2, 3, or 4 manageable installments. Instead of losing that customer, you convert them while maintaining your full pricing power.

The Flexible Payment Revolution

The payment landscape has fundamentally shifted. Nearly 4 in 5 merchants plan to improve their installment payment capabilities because consumer behavior has changed permanently.

Market Growth:

- BNPL usage increased 400% globally since 2018, growing 17% annually through 2028

- BNPL now represents 5% of global e-commerce transactions, projected to reach 9% by 2027

- An estimated 86.5 million people in the U.S. used BNPL in 2024, up 6.92% year-over-year

Consumer Expectations:

- 88% of consumers want to know about installment options before or during checkout

- 60% of BNPL users are under 40 years old

- 50% of consumers would switch merchants for flexible payment options

This isn't a trend, it's the new standard. Customers expect payment flexibility, and businesses that don't offer it are losing sales to competitors who do.

Measurable Business Impact

Conversion Rate Improvements

Price sensitivity is the #1 reason customers abandon purchases. Pay-in-Tranches directly addresses this:

- RBC Capital Markets found BNPL increases retail conversion rates from 20% to 30%

- Flexible payment options reduce cart abandonment by up to 40%

- Up to 40% of BNPL sales come from new customers to the retailer

Revenue Growth

Flexible payments don't just convert more customers, they increase spending per customer:

- BNPL results in 85% higher average order value than traditional payment methods

- BNPL omnichannel shoppers spend 72% more per transaction

- The average BNPL purchase amount grew 11.6% from $135 in 2021 to $142 in 2022

Customer Satisfaction and Retention

Happy customers become repeat customers:

- BNPL customer satisfaction rose 16 points year-over-year

- Flexible payment options boost Customer Lifetime Value (CLV) through enhanced satisfaction and loyalty

- BNPL customers are engaged over longer periods and make more frequent purchases

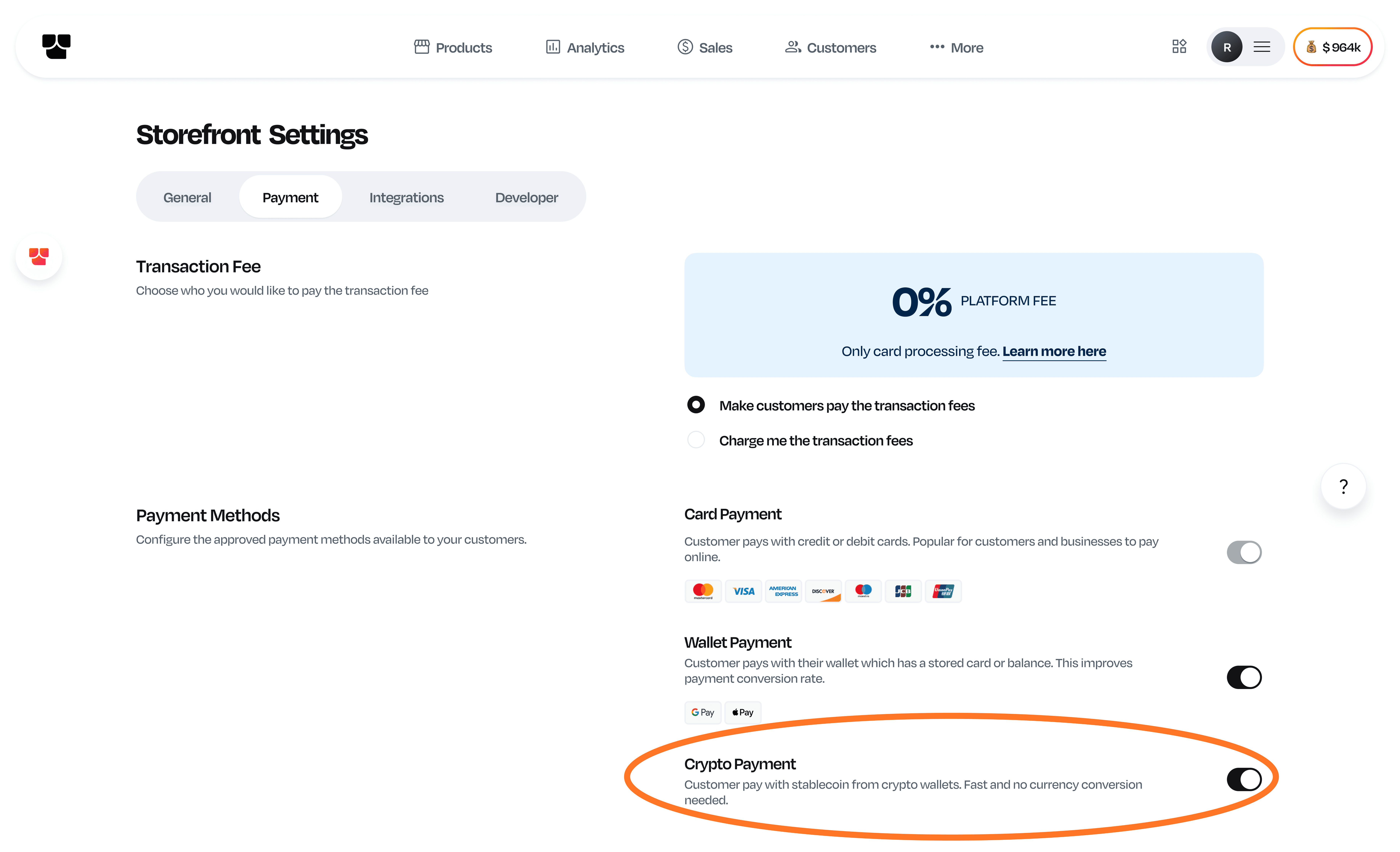

How Pay-in-Tranches Works

Payment Structure Options

Installment Splits:

- 2 payments: 50% at purchase, 50% later

- 3 payments: 33% at purchase, two additional payments

- 4 payments: 25% at purchase, three additional payments

Flexible Intervals:

- Monthly payments for ongoing programs

- Quarterly payments for seasonal offerings

- Custom intervals based on your business model

Automated Management:

- Automatic charge processing

- Payment failure handling

- Customer notification system

- Real-time status updates

Advanced Features

Smart Analytics Dashboard:

- Payment success rates by installment option

- Customer payment behavior patterns

- Revenue forecasting based on scheduled payments

- Churn prediction for incomplete payment plans

Risk Management:

- Automated credit checks for larger amounts

- Payment failure retry logic

- Flexible grace periods

- Customer communication workflows

Integration Capabilities:

- Seamless checkout experience

- Mobile-optimized payment flows

- Multiple currency support

- Third-party tool integrations

Industry-Specific Applications

Online Education and Courses

Educational purchases are perfect for installment payments because they're high-value investments in personal development:

- 59% of installment users manage finances better with big-ticket educational purchases

- Course creators can offer semester-long programs with monthly payments

- Certification programs become accessible to working professionals

- Corporate training packages can be structured around quarterly budgets

Digital Products and Software

High-value digital products benefit significantly from payment flexibility:

- Template bundles and design assets appeal to budget-conscious creatives

- Software licenses can be paid over time, reducing barrier to entry

- Digital marketing tools and courses convert better with installment options

- Subscription products can offer annual plans with quarterly payments

Services and Consulting

Professional services often face price objections that installments can overcome:

- High-value consulting packages become more accessible

- Coaching programs can align payments with session schedules

- Done-for-you services can split payments across project milestones

- Retainer agreements can offer flexible payment structures

E-commerce and Physical Products

Even traditional retail benefits from payment flexibility:

- Home & furniture is the most popular BNPL category, with 42% of users making these purchases

- Electronics and gadgets see higher conversion with installment options

- Seasonal products can offer payments aligned with usage periods

Customer Psychology and Payment Behavior

Understanding why customers choose installment payments helps optimize your offering:

Financial Management

75% of paycheck-to-paycheck consumers use flexible payment plans for financial relief, but it's not just about financial stress. Many customers use installments for:

- Budget control: Spreading costs across pay periods

- Cash flow management: Preserving liquid funds for emergencies

- Purchase timing: Buying when needed, paying when convenient

Convenience and Preferences

18% of financially secure consumers use installment plans for convenience, with 15% seeking rewards. This shows that payment flexibility appeals across income levels.

Psychological Factors

- Reduced payment pain: Smaller amounts feel more manageable

- Immediate gratification: Get the product now, pay later

- Risk reduction: Lower initial commitment reduces purchase anxiety

Implementation Best Practices

Display Strategy

More than 60% of consumers prefer to know about installment options before deciding to buy. This means:

- Product pages: Show installment amounts prominently

- Pricing displays: "Starting at $25/month" instead of "$100 total"

- Marketing materials: Feature payment flexibility in your messaging

- Email campaigns: Highlight installment options for abandoned carts

User Experience Optimization

- Simple selection: Clear options without overwhelming choices

- Transparent terms: No hidden fees or confusing conditions

- Easy management: Customer dashboard for payment tracking

- Clear communication: Automated reminders and updates

Customer Support

- Educational content: Help customers understand installment benefits

- Payment assistance: Support for customers with payment issues

- Flexible policies: Options for payment rescheduling when needed

- Proactive communication: Updates on upcoming payments

Competitive Advantages

Market Differentiation

In crowded markets, payment flexibility becomes a key differentiator:

- Price positioning: Compete with lower-priced alternatives by reducing upfront cost

- Customer acquisition: Attract price-sensitive customers who would otherwise choose competitors

- Brand perception: Position yourself as customer-centric and accessible

- Market expansion: Reach customers who couldn't afford your products previously

Customer Loyalty

BNPL customers are more engaged and make more frequent purchases, leading to:

- Higher retention rates: Customers appreciate payment flexibility

- Increased referrals: Satisfied customers recommend your business

- Cross-selling opportunities: Customers comfortable with installments buy more

- Reduced price shopping: Less likely to compare prices when payment is comfortable

Risk Management and Best Practices

Financial Considerations

- Cash flow impact: Understand how installments affect your working capital

- Payment failure rates: Plan for typical 5-10% payment default rates

- Customer screening: Basic qualification criteria for larger installment amounts

- Reserve planning: Maintain reserves for payment processing delays

Operational Setup

- Clear policies: Define installment terms and conditions

- Customer communication: Automated systems for payment reminders

- Support processes: Procedures for handling payment issues

- Integration testing: Ensure seamless checkout experience

The market momentum is undeniable. BNPL is projected to grow at 9% CAGR through 2027, driven by:

- Generational shift: Millennials and Gen Z prefer flexible payment options

- Economic uncertainty: Consumers seek financial flexibility during volatile times

- Technology advancement: Better payment processing and risk management tools

- Merchant adoption: More businesses recognizing competitive necessity

Businesses that don't offer flexible payments risk becoming irrelevant as customer expectations evolve. Pay-in-Tranches positions you ahead of this curve.

Getting Started with Pay-in-Tranches

The setup process is straightforward:

- Choose your installment options: Decide on 2, 3, or 4 payment splits

- Set payment intervals: Monthly, quarterly, or custom schedules

- Configure your checkout: Integrate installment options into your sales flow

- Update your marketing: Highlight flexible payment options in your messaging

- Monitor and optimize: Track conversion improvements and customer feedback

Your competitors are already offering flexible payments. Every day you wait, you're losing sales to businesses that understand modern customer expectations.

Pay-in-Tranches gives you the tools to compete effectively: higher conversion rates, increased average order values, improved customer satisfaction, and predictable revenue streams.

The question isn't whether to offer flexible payments, it's whether you'll implement them before or after your competitors capture your price-sensitive customers.

.jpg)